Every month, your payroll team deducts CIT and EPF from employee salaries, but can anyone in your organisation clearly explain the difference between the two? Most cannot. And that silent confusion quietly costs businesses wrong contribution structures, missed compliance obligations, and employees who arrive at retirement with far less than they were promised.

Both CIT (Citizen Investment Trust) and EPF (Employees Provident Fund) are government-backed savings institutions. Both appear on payslips. Both offer tax deduction benefits. But they are fundamentally different tools built for different purposes, and treating them as interchangeable is an HR mistake your organisation cannot afford.

This guide breaks down exactly what each fund is, what is the difference between CIT and EPF, their benefits, the calculation methods, and how each makes sense for your workforce.

What Is CIT (Citizen Investment Trust)?

CIT stands for Citizen Investment Trust, known in Nepali as Nagarik Lagani Kosh. It is a government-owned savings and investment institution established on 18th March 1991 under the Citizen Investment Trust Act, 2047. The Government of Nepal runs and oversees it, making it one of the most trusted financial bodies in the country.

The main goal of CIT is to help Nepali citizens save money, grow it over time, and be financially secure when they retire. It is open to salaried employees, self-employed individuals, and even private citizens who want a safe place to invest for the future.

CIT takes the money contributed by hundreds of thousands of members and invests it in infrastructure, capital markets, and hydropower projects across Nepal. This means your savings are not sitting idle, they are actively working and growing.

Today, CIT serves around 350,000 participants in its Employee Savings Growth Retirement Fund alone, with offices in Kathmandu, Pokhara, Biratnagar, Butwal, Attariya, and Surkhet.

What Is EPF (Employees Provident Fund)?

EPF stands for Employees Provident Fund, officially known in Nepali as Karmachari Sanchaya Kosh. It was established under the Employees Provident Fund Act, 2019 B.S. (1962 A.D.) and is one of the oldest and most trusted retirement savings institutions in Nepal. It works under the oversight of the Ministry of Finance and covers employees in the government, public enterprises, and private sector.

The history of EPF in Nepal goes back to 1934, when the first savings fund was set up for army personnel during the Rana Regime. Since then, it has grown significantly. Today, EPF manages provident funds for over 600,000 employees across the country.

EPF is recognised as an approved retirement fund under Nepal's Income Tax Act, 2058. This means employees who contribute to EPF can claim income tax deductions on their contributions and enjoy tax benefits on withdrawals.

One of the biggest advantages of EPF is its government-backed interest guarantee. No matter what happens in the market, the Government of Nepal guarantees a minimum of 3% annual interest on every member's account, giving employees a reliable, risk-free foundation for their retirement savings.

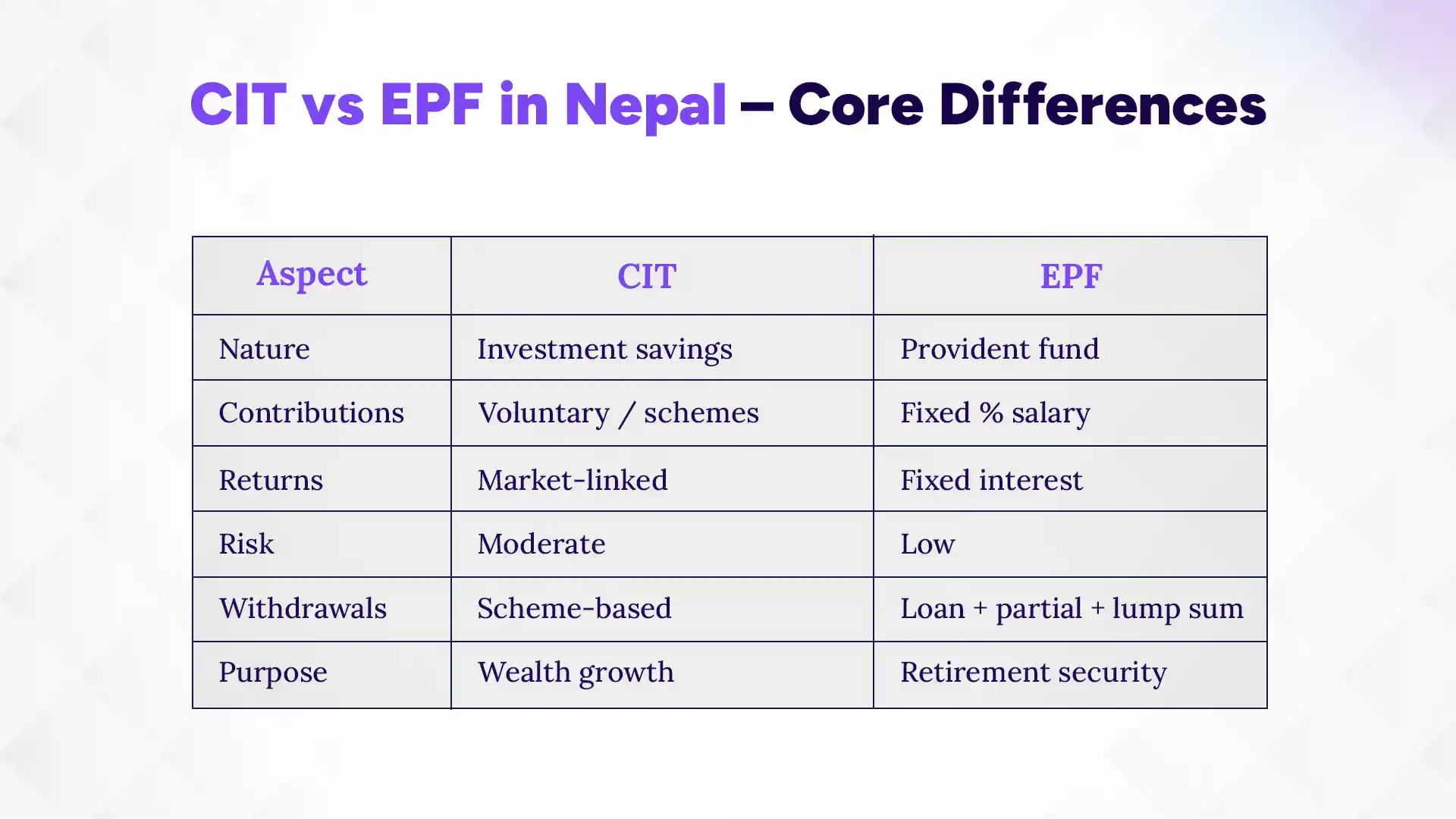

CIT vs EPF in Nepal – Comparing the Core Differences

CIT and EPF are both government-backed savings funds in Nepal, but they work very differently. EPF is a mandatory provident fund that guarantees stable retirement savings, while CIT is an investment trust that focuses on growing your money over time. Moreover, EPF requires fixed contributions from both employer and employee, whereas CIT offers more flexible, scheme-based options with returns tied to investment performance.

Understanding these core differences helps employers structure payroll correctly, stay compliant, and guide employees toward smarter retirement decisions, so let's break down each key difference one by one:

1. Nature: Investment Savings vs Provident Fund

The most fundamental distinction between CIT and EPF is what each institution actually is at its core. EPF is a provident fund, a structured retirement savings mechanism governed by a specific Act, with fixed contribution rules, government-guaranteed minimum returns, and a clear mandate to preserve and grow employee savings for retirement.

CIT is an investment and savings trust. A government-owned body that runs multiple financial schemes including retirement plans, mutual funds, and pension programs, with returns tied to investment performance and fund profit.

This distinction shapes every practical difference that follows, from how contributions are made, to how returns are determined, to how flexible withdrawals are, to who benefits most from each.

2. Contributions Type & Method

EPF contributions are non-negotiable for eligible employees and employers. Both the employer and the employee contribute exactly 10% of the employee's basic salary each month. There is no room for discretion, adjustment, or opt-out. Once you’ve chosen EPF as an eligible employer in Nepal with 10 or more employees, this deduction is your legal obligation under the Employees Provident Fund Act and the Labour Act, 2074.

CIT contributions, by contrast, depend entirely on which scheme the employee participates in. For organisations enrolled in the Employee Savings Growth Retirement Fund (ESGRF), contributions follow a scheme-defined structure through payroll deduction. For individuals joining CIT's Citizen Pension Scheme voluntarily, contributions can start at as little as NPR 500 per month and can be made monthly, quarterly, half-yearly, or yearly. This flexibility is a genuine advantage for employees who want to top up their retirement savings beyond what EPF provides, but it also means CIT is less of a compliance certainty for employers and more of an employee benefit option.

3. Returns: Fixed Interest vs Performance-Linked Growth

EPF gives you a fixed, predictable return. For FY 2082/83, the EPF interest rate is 5.00%, as declared by the government, guaranteed, and the same for every member. There are no surprises.

CIT returns depend on how well the fund's investments perform that year. For FY 2024/25, ESGRF participants are earning 6.50%, which is higher than EPF right now. But that number can go up or down depending on the year. In stronger years, CIT pays a bonus on top of the base rate. In weaker years, that bonus may shrink or disappear entirely.

The simple way to think about it: EPF is predictable, CIT has more upside.

If your employee has 20 or more years until retirement, CIT's growth potential is worth considering. If they are retiring soon and need certainty, EPF's fixed rate is the safer choice.

4. Risk: Low vs Moderate

EPF is about as safe as it gets. It is government-managed, legally protected, and no creditor, not even the government itself can touch the money in your EPF account. Your principal and interest are completely secure.

CIT carries a small amount of risk because its returns depend on investment performance. In a bad year, returns may be lower than expected. But "moderate risk" does not mean dangerous. CIT is still a government-backed institution with a conservative investment approach. It is far safer than private mutual funds or investing in the stock market yourself.

5. Withdrawals: Flexible vs Scheme-Dependent

EPF gives you clear, structured withdrawal options. You can take a loan for house construction (up to Rs. 1 crore) or renovation (up to Rs. 30 lakhs), make partial withdrawals under qualifying conditions, and receive your full lump sum when you retire or leave your job. EPF even continues earning interest for up to six years after retirement before you withdraw.

CIT withdrawals depend on which scheme you are enrolled in. ESGRF members can borrow against their balance, while Citizen Pension Scheme members receive regular pension payouts after retirement. For HR teams, this means you need to know exactly which CIT scheme each employee is in before advising them on withdrawals.

Overall, EPF withdrawals are simpler and more uniform. CIT withdrawals vary by scheme.

6. Purpose: Retirement Security vs Wealth Growth

EPF has one job. To make sure your employees have money when they retire. Everything about it is designed around that single goal: mandatory contributions, fixed interest, legal protections.

CIT has a broader goal. It helps employees grow their wealth over time, not just save it. This is why CIT offers mutual funds, pension plans, and investment-linked schemes alongside basic retirement savings. It is built for employees who want their money to do more than sit and accumulate at a fixed rate.

So the bottom line is, EPF secures your retirement. CIT grows your wealth.

Ready to Simplify CIT and EPF Management?

Automate contributions, payroll calculations, and compliance with a smarter HRMS solution.

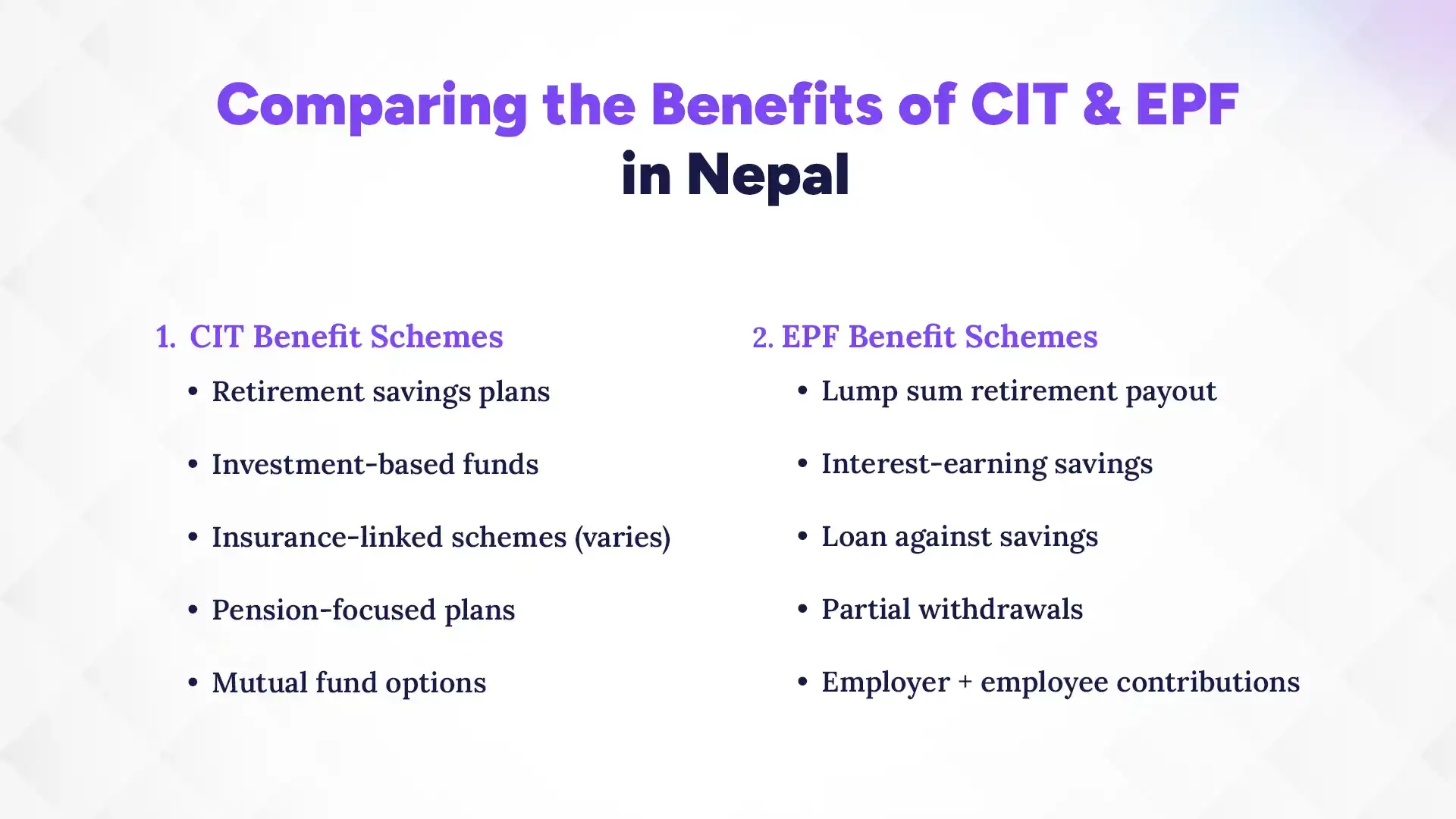

Comparing the Benefits of CIT and EPF in Nepal

Both CIT and EPF offer strong benefits to employees, but they do so in very different ways. CIT gives employees more options for growth and flexibility, while EPF focuses on stable, reliable retirement savings. Each fund has its own set of schemes and features worth understanding. Here is a clear breakdown of what each one actually offers.

1. CIT Benefit Schemes

CIT's value to employees is not confined to a single payout at retirement. It offers a range of benefit mechanisms that address different financial goals across an employee's career. Here are all the major CIT schemes you must know about:

Employee Savings Growth Retirement Fund (ESGRF)

This is CIT's main workplace retirement scheme. Employees contribute monthly through payroll, and the money grows with annual interest plus a profit-sharing bonus. For FY 2024/25, ESGRF participants are earning 6.50%, which is one of the best rates among government-backed savings tools in Nepal.

Citizen Pension Scheme

Instead of a one-time lump sum, this scheme pays a regular monthly income after retirement, just like a pension. It has been running since 2019 and is especially valuable for private sector employees who otherwise have no access to a monthly pension. If the contributor passes away, their spouse continues receiving pension benefits, making it a genuine family protection tool.

Insurance-Linked Funds

CIT manages dedicated insurance funds for civil servants, teachers, army, police, and armed police personnel. These schemes combine retirement savings with life insurance coverage, so employees are protected both during their career and after it.

Mutual Fund Programs

For employees who want their savings to grow faster, CIT offers mutual fund options linked to Nepal's capital markets. These are best suited for employees with a longer investment horizon and a slightly higher risk tolerance who want returns beyond what fixed-rate schemes provide.

Loan Facility

CIT members can borrow against their savings at the rates of 8.50% for educational loans, 8.50% for housing loans, and 9.00% for simple loans. This makes CIT useful throughout an employee's career, not just at retirement.

2. EPF Benefit Schemes

EPF's benefits are more concentrated but deeply reliable. The full accumulated balance of both employee and employer contributions, plus all interest credited annually is paid out upon retirement or separation from service. For an employee who has contributed consistently over 20 or 30 years, this can represent a substantial financial safety net.

Lump Sum Retirement Payout

When an employee retires or leaves their job, they receive their full accumulated balance. Every rupee contributed by them and their employer, plus all interest earned over the years in one payment. For someone who has contributed consistently for 20 to 30 years, this is a substantial financial safety net. However, you’ll have to pay a certain tax on withdrawal.

Guaranteed Interest on Savings

EPF savings earn a government-declared interest rate every year. Currently, this is 5.00% for FY 2082/83, with a guaranteed minimum of 3% no matter what happens in the market. Employees do not need to monitor anything or make any investment decisions. The money simply grows, year after year.

Loans Against EPF Balance

EPF members can borrow significant amounts against their savings at rates set by the EPF board, which is generally lower than commercial bank lending rates. There’s a limit up to Rs. 1 crore for house construction nd up to Rs. 30 lakhs for house renovation.

Employer Contribution Match

Every month, your employer is legally required to deposit 10% of the employee's basic salary into their EPF account, equal to what the employee contributes. Over a 30-year career, this doubles the savings base before interest is even calculated. No voluntary savings scheme can replicate this automatic, employer-funded advantage.

Legal Protection of Savings

EPF savings are fully protected by law. No creditor, court, or even the government can claim or attach the money in an employee's EPF account. No matter what financial difficulties an employee faces in their personal or professional life, their EPF balance remains completely safe.

How to Calculate CIT and EPF Contributions in Nepal?

Calculating CIT and EPF sounds simple, but managing them correctly across multiple employees every single month is where most employers run into trouble. Different salary levels, different schemes, and different contribution histories all add up quickly without a proper system in place.

1. How to Calculate EPF in Nepal?

EPF is straightforward. Both the employer and employee each contribute 10% of the employee's basic salary, making the total monthly deposit 20% of basic salary. Only basic salary counts. Bonuses and allowances are excluded.

Example: Employee's basic salary = NPR 30,000

- Employer contribution = NPR 3,000

- Employee contribution = NPR 3,000

- Total EPF deposit = NPR 6,000 per month

Over 12 months, that is NPR 72,000 in contributions, before interest. At the current rate of 5.00% (FY 2082/83), the compounding effect over a long career adds up significantly.

One important rule for employers: if you fail to deposit EPF on time for any reason, you are legally required to pay an additional 10% of the employee's basic salary as a penalty. Non-compliance is not just a compliance risk, it is an automatic financial cost.

2. How CIT Is Calculated

CIT does not follow a fixed percentage like EPF. The contribution amount depends entirely on which scheme the employee is enrolled in.

For ESGRF participants, the employer and employee agree on a contribution amount as part of the employment arrangement, and deductions are made monthly through the employer's bank or CIT's online system.

For Citizen Pension Scheme participants, contributions are voluntary and start at a minimum of NPR 500 per month, with no employer-matching obligation unless the organisation separately agrees to it.

For tax purposes, CIT contributions are counted as part of the approved retirement fund deduction, along with EPF and SSF. This is subject to the combined ceiling of NPR 500,000 or one-third of assessable income, whichever is lower.

3. Why Manual CIT & EPF Calculation Becomes a Challenge

Even though EPF uses a fixed formula, managing payroll for multiple employees gets complicated fast. Common problems include:

- Calculation errors every time an employee gets a salary increment

- Difficulty tracking which CIT scheme each employee is enrolled in

- Time-consuming monthly reconciliation across both funds

- Compliance risk if EPF deposits are delayed or miscalculated

The numbers add up quickly. A NPR 500 monthly error per employee across just 50 employees means NPR 25,000 lost per month, and NPR 3 lakhs per year! This is why it is always wise to use reliable HR payroll software to not only simplify but to be able to put confidence in your calculation and salary processing process.

4. How HR Software Simplifies CIT and EPF Management

This is where modern HR and payroll software stops being a nice-to-have and becomes a necessity for growing Nepali businesses. A good HR system will:

- Automatically calculate EPF contributions based on current basic salary

- Update calculations instantly when salaries change

- Track each employee's CIT scheme and contribution details

- Generate monthly deposit reports for both EPF and CIT

- Flag compliance issues before they become penalties

- Maintain a clean audit trail for tax filing and reporting

Instead of juggling spreadsheets, everything is in one place, saving your HR team hours every month and protecting your business from costly errors.

5. Which Is the Best HR Software for Payroll with CIT and EPF Integration in Nepal?

Pace HRMS is one of Nepal's trusted HR and payroll software with full CIT and EPF integration, built with local compliance in mind. It takes the complexity out of managing CIT and EPF contributions by automating the entire payroll process. from salary calculation to fund deductions.

These are the functions and advantages you enjoy with Pace HRMS:

- Automated salary processing with built-in CIT and EPF calculations

- Employer dashboard to track and manage all fund contributions

- Employee self-service to check balances and download salary slips

- Payroll compliance updated with Nepal's latest tax and contribution rules

- Leave and attendance management integrated directly with payroll

- Digital employee records and onboarding from day one

- Automated tax deductions including TDS and retirement fund calculations

For employers who are tired of chasing contribution errors, reconciling spreadsheets every month, and worrying about EPF penalties, Pace HRMS brings everything under one roof. Clean, accurate, and compliant.

Can You Have Both CIT and EPF?

Yes, and for many employees in Nepal, having both is not just permissible but genuinely advisable.

EPF gives employees a stable, employer-matched, government-guaranteed foundation. CIT adds a growth layer on top, with higher return potential, pension income options, and mutual fund exposure. Together, they cover what neither can fully deliver alone: security and growth in one balanced retirement strategy.

For employers, supporting both sends a clear message to your workforce that you care about their long-term financial wellbeing, not just minimum compliance. In a competitive Nepali labour market, that kind of employee-first approach matters for retention.

From a tax perspective, contributions to both EPF and CIT fall under the same approved retirement fund deduction ceiling. Which is NPR 500,000 or one-third of assessable income, whichever is lower. Most mid-income employees have enough room within this limit to maximise contributions to both without losing any tax benefit.

Pros and Cons of CIT (Citizen Investment Trust)

CIT is a government-backed investment trust that offers more than just retirement savings. It gives employees a chance to grow their wealth over time. Because returns are linked to fund performance, CIT can outperform EPF in good years, but offers less predictability in leaner ones. It is best suited for employees who want flexibility, higher long-term returns, and a broader range of savings options beyond a fixed monthly deduction.

| Pros | Cons |

|---|---|

| Higher return potential of ESGRF at 6.50% for FY 2024/25 | Returns not guaranteed, and varies by year and scheme |

| Money is actively invested and put to work | Market performance directly affects how much you earn |

| Multiple schemes for different goals and risk levels | Requires financial awareness to choose the right plan |

| Citizen Pension Scheme offers monthly income after retirement | Less predictable for employees close to retirement |

| Complements EPF with a different return mechanism | Not ideal for those who prefer a hands-off approach |

CIT is a strong choice for employees who are comfortable with performance-linked returns and want to build wealth beyond basic retirement savings. It works best for private sector employees with 15 or more years until retirement, individuals who want a monthly pension rather than just a lump sum, and those who want to grow their savings through a safe, government-managed investment vehicle. It is not the right fit for risk-averse employees, those nearing retirement, or anyone who simply wants a guaranteed, no-decisions savings structure.

Pros and Cons of EPF (Employees Provident Fund)

EPF is Nepal's most established retirement savings system. It does not promise the highest returns, but it promises certainty, which is something no investment-linked fund can fully match. It is the financial bedrock that every formal sector employee in Nepal has access to, regardless of financial literacy or income level.

| Pros | Cons |

|---|---|

| Fixed 5.00% interest for FY 2082/83, no surprises | Lower returns than CIT's ESGRF (6.50%) |

| Government guarantees a minimum 3% return always | Limited wealth growth potential over the long term |

| Employer matches your 10%, doubling your savings base | Contribution rate is fixed so no flexibility to adjust |

| Legally protected, no creditor can touch your balance | No mutual fund or equity exposure options |

| Loans available for housing and other qualifying needs | Focused only on retirement, not broader wealth building |

EPF is the right foundation for employees who value certainty and stability over high returns. It is ideal for government and public enterprise workers, employees in the early stages of their career who benefit most from decades of compounded employer-matched contributions, and risk-averse individuals who want guaranteed savings without making any financial decisions. It may not fully satisfy high-income earners or long-term investors who want their money to grow faster, and for those employees, pairing EPF with CIT is the smarter approach.

Conclusion

At their core, CIT and EPF represent two different philosophies about how employees should prepare for the future. CIT and EPF are not competitors, they are complements.

EPF is stability: a government-guaranteed, employer-matched foundation that every formal sector employee in Nepal can count on. CIT is growth: a flexible, investment-linked layer that helps employees build real wealth beyond the retirement minimum.

For employers and HR managers, understanding this difference is not just useful background knowledge, it directly affects your payroll accuracy, compliance obligations, and your ability to support your workforce's long-term financial wellbeing.

The organisations that get this right are the ones that attract better talent, retain them longer, and build workplaces where employees feel genuinely taken care of, not just legally covered.

Are you seeking for a more effective and efficient way of handling CIT, EPF, SSF, and payroll? Explore how an HR payroll software can benefit you in 2026.