We all love payday. But when you look at your payslip, do you ever stare at that "Provident Fund" cut and wonder where your money actually goes?

For many workers in Nepal, the Employee Provident Fund just feels like a confusing math problem that makes your monthly take-home pay smaller.

On the flip side, HR teams are constantly stressed trying to manage these funds. Calculating exact amounts, matching employer shares, and following strict government rules is a massive headache every single month.

So, what exactly is a Provident Fund (PF)? More importantly, why does it matter so much? Is all this hassle and commitment even worth it?

In this guide, we will explore exactly what PF is, how it builds your future wealth, and the best way for businesses to manage it without the monthly chaos. Let's dive in!

What is Provident Fund (PF) in Nepal?

A Provident Fund (PF) is a formal retirement savings program set up for employees. In Nepal, this fund is managed by a government body known as the Karmachari Sanchaya Kosh (KSK), or the Employee Provident Fund (EPF). Its primary purpose is to help employees save money throughout their careers to ensure they have a financial safety net after retirement.

So, how does it work? It’s quite simple. Every month, 10% of your salary is automatically taken out and put into your PF account. Then, your employer contributes an equal amount, which is another 10% of your salary to the same account. This immediately doubles the amount you are saving each month.

This collected amount doesn’t just sit there; it earns interest over time, helping your fund grow even more. This whole system is designed to provide you with a significant lump-sum payment when you retire or decide to leave your job. It’s a fantastic way to ensure you have financial security waiting for you down the road.

What is a PF Account?

A PF account is simply the specific account where your retirement funds are safely kept. Every month, a set portion of your salary is deposited directly into this account. Right alongside that, your employer adds the exact same amount to match your contribution.

Because both you and your company are putting money in, the balance grows steadily over time. The entire purpose of this account is focused on long-term savings. It locks this money away so you can build a strong financial foundation for your life after work.

What is an Employee Provident Fund (EPF)?

The Employee Provident Fund (EPF) is the official government organization responsible for managing all PF accounts in Nepal. You will often hear it referred to by its Nepali name, Karmachari Sanchaya Kosh (KSK). The EPF’s main job is to protect your deposited money, manage the funds properly, and make sure your savings earn interest every year.

Initially, this organization was created specifically for government workers, the army, and the police force. Today, however, its reach is much broader. The EPF now covers a wide range of sectors, including public school teachers, employees of public corporations, and workers in many private companies across Nepal.

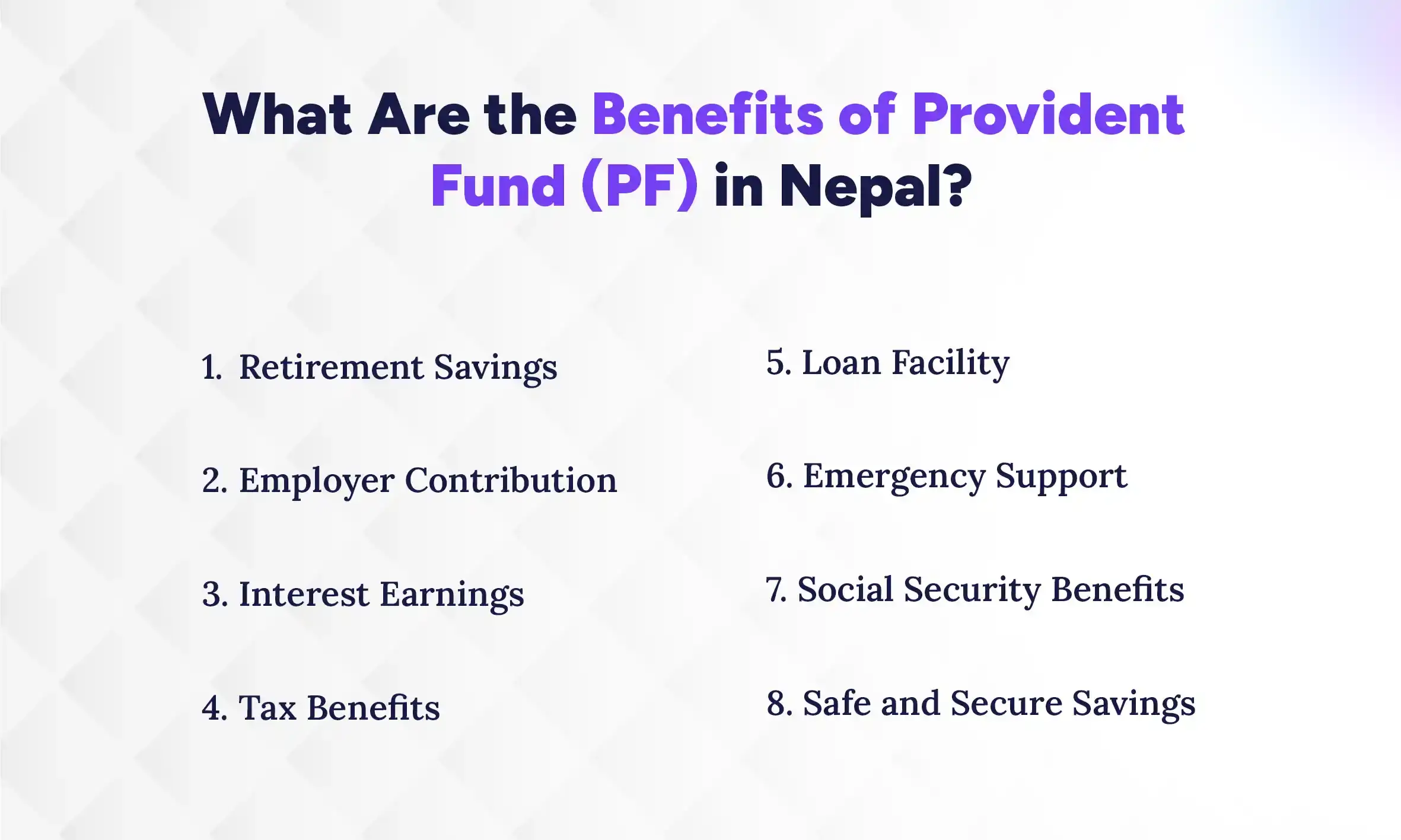

What Are the Benefits of Provident Fund (PF) in Nepal?

The main benefits of a Provident Fund (PF) in Nepal include building a large retirement fund, getting free matching money from your employer, earning compound interest, and saving on annual taxes. Because this money is automatically deducted from your salary and grows over time, it forces you to build wealth without even trying. Let’s look closely at how each of these specific benefits works to secure your financial future.

1. Retirement Savings

The core purpose of your PF is to build a massive financial cushion for your old age. By saving a small piece of your paycheck every month, you create a huge pile of cash over decades. When you finally stop working, this fund gives you the cash you need to live comfortably. Therefore, starting early means you will have much more money waiting for you later.

2. Employer Contribution

One of the best perks of a PF is the free money you get from your boss. Whenever you put 10% of your salary into the fund, your employer must match that exact amount. Because of this rule, your monthly savings instantly double without any extra effort from you. This matching contribution is essentially a guaranteed 100% return on your investment right from day one.

3. Interest Earnings

Your PF money does not just sit in an account doing nothing. The Employee Provident Fund (EPF) pays a fixed annual interest rate on your total balance. Plus, this interest compounds every year, meaning you earn money on the interest you already made. Over time, this compounding effect makes your total savings grow much faster than a standard bank account.

4. Tax Benefits

Putting money into a PF directly lowers the amount of income tax you have to pay each year. In Nepal, the government lets you deduct your PF contributions from your taxable income up to a certain limit. As a result, you get to keep more of your hard-earned salary in your pocket right now. Ultimately, this makes the PF a smart tool for legally reducing your tax bill.

5. Loan Facility

You do not have to wait until retirement to use your PF money. If you want to buy a house, pay for college, or cover a big expense, you can borrow directly from your fund. Since you are borrowing your own money, the interest rates are very low and approval is quick. This feature gives you easy access to cash while keeping your retirement goals on track.

6. Emergency Support

Life is unpredictable, but your PF acts as a strong safety net during tough times. If you face a sudden medical crisis or lose your job, you can withdraw a portion of your savings to stay afloat. Instead of taking on high-interest debt from outside lenders, you can tap into this emergency lifeline. Therefore, your PF protects you from financial ruin when unexpected disasters strike.

7. Social Security Benefits

Beyond just saving money, the EPF provides valuable insurance and social security coverage for you and your family. If an active contributor faces a severe accident or passes away, the fund pays out a special relief amount to their dependents. Additionally, it offers maternity benefits and medical claim support for certain illnesses. This extra layer of protection brings peace of mind to your entire household.

8. Safe and Secure Savings

Your money is extremely safe because the EPF is fully backed and managed by the government of Nepal. Unlike risky stock market investments, your principal amount and your guaranteed interest are completely protected from market crashes. You will never have to worry about losing your life savings due to bad business deals. This strict government oversight ensures your money is always there when you need it.

Ready to Simplify Provident Fund Management?

Automate PF contributions, payroll calculations, and compliance with a smarter HRMS solution.

How Does Provident Fund Work in Nepal?

The working of provident fund is actually a very straightforward system once you know the basics.The whole process begins as soon as you are hired by a registered organization. Your employer takes the first step by officially registering you with the EPF and opening a unique PF account in your name. You do not have to worry about going to the government office yourself.

Once your account is set up, the monthly cycle begins. When payday arrives, your employer calculates your basic salary. They automatically deduct a specific percentage from your paycheck. Immediately after that, the employer adds the exact same amount from their own company funds to match your deduction.

Next, your employer takes this combined money and deposits it directly into your EPF account. They are legally required to do this every single month. Finally, the EPF takes over the job. They securely hold your funds, invest the money, and add interest to your total balance every year.

Let’s break down exactly how the Provident Fund operates in Nepal. It is a straightforward system that involves three main parties: you (the employee), the employer, and the Employee Provident Fund (EPF) office. Working together, these three make sure your retirement savings are collected, managed, and grown safely over your career.

1. What is the PF Contribution in Nepal?

The core of the PF system is your monthly contribution. Normally, 10% of your basic salary is deducted each month. Your employer then matches this by adding another 10% from their side.

But what exactly is a "basic salary"? It is your fixed base pay before any extra allowances, bonuses, or overtime are added. So, the 10% deduction is calculated only on that base amount, not your total take-home pay.

There is also a slightly different setup called the Contributory Pension Scheme (CPS) for certain employees. Under this specific program, both you and your employer contribute 6% each instead of the standard 10%.

2. Who is Eligible for a Provident Fund Account?

In 2026, employees working in public enterprises, teachers, and staff in registered private companies are all eligible for a provident fund account. Originally, this fund was mainly set up for government employees, the army, and the police force. Today, it covers a lot more ground.

If you work for a registered company in Nepal, your employer is legally responsible for enrolling you in the fund. They must set up your account and make sure the monthly deposits happen on time. You do not have to worry about dealing with the initial paperwork yourself.

3. How Does Your PF Money Grow Over Time?

Watching your account balance increase is one of the best parts of the system. It all starts with those automatic monthly deductions. Because your employer matches your deposit, your savings double instantly without any extra effort from you.

Over the years, this money really piles up. Thanks to the power of long-term compounding, the interest you earn also starts earning its own interest. This means your money grows much faster the longer you leave it in the account.

4. How Much Interest Does EPF Pay on Your Savings?

The Employee Provident Fund (EPF) safely invests it to earn returns. Every year, they distribute interest directly into your account. While the exact rate changes slightly based on the economy, it usually stays at a very competitive rate, often around 7% to 8%.

On top of the regular interest, the EPF sometimes distributes a bonus or a share of their annual profits. This extra boost gets added directly to your total balance, helping your retirement fund get even larger over your career.

5. When Can You Withdraw or Take a Loan from Your PF?

The main goal of PF is saving for retirement. However, life happens, and sometimes you need access to your funds earlier. You can usually withdraw your total saved amount when you retire, resign, or officially leave your job.

You do not always have to quit your job to use this money, though. The EPF offers some really helpful loan facilities. If you have been contributing regularly, you can take out a loan against your own savings. People often use these loans to buy a house, pay for higher education, or cover sudden emergencies. It is a great way to get cash at a lower interest rate without touching your actual savings.

How is Provident Fund Calculated?

Your Provident Fund is calculated by taking exactly 10% of your monthly basic salary (before any extra allowances) and combining it with a matching 10% contribution from your employer. This means a total of 20% of your basic salary goes straight into your PF account each month.

Example of Provident Fund Calculation in Nepal

Let’s look at a concrete example. To find your exact contribution, you only need to look at your basic salary, which is your pay before any allowances or bonuses. Suppose your basic salary is NPR 30,000 per month.

Here is exactly how the monthly breakdown and annual accumulation work out:

| Description | Calculation | Amount (NPR) |

|---|---|---|

| Employee Monthly Contribution (10% deduction) | 30,000 × 10% | 3,000 |

| Employer Monthly Contribution (10% match) | 30,000 × 10% | 3,000 |

| Total Monthly PF Deposit | 3,000 + 3,000 | 6,000 |

| Total Annual Accumulation (Before interest) | 6,000 × 12 | 72,000 |

So, on a basic salary of NPR 30,000, exactly NPR 72,000 is saved into your PF account by the end of one year, purely from base contributions.

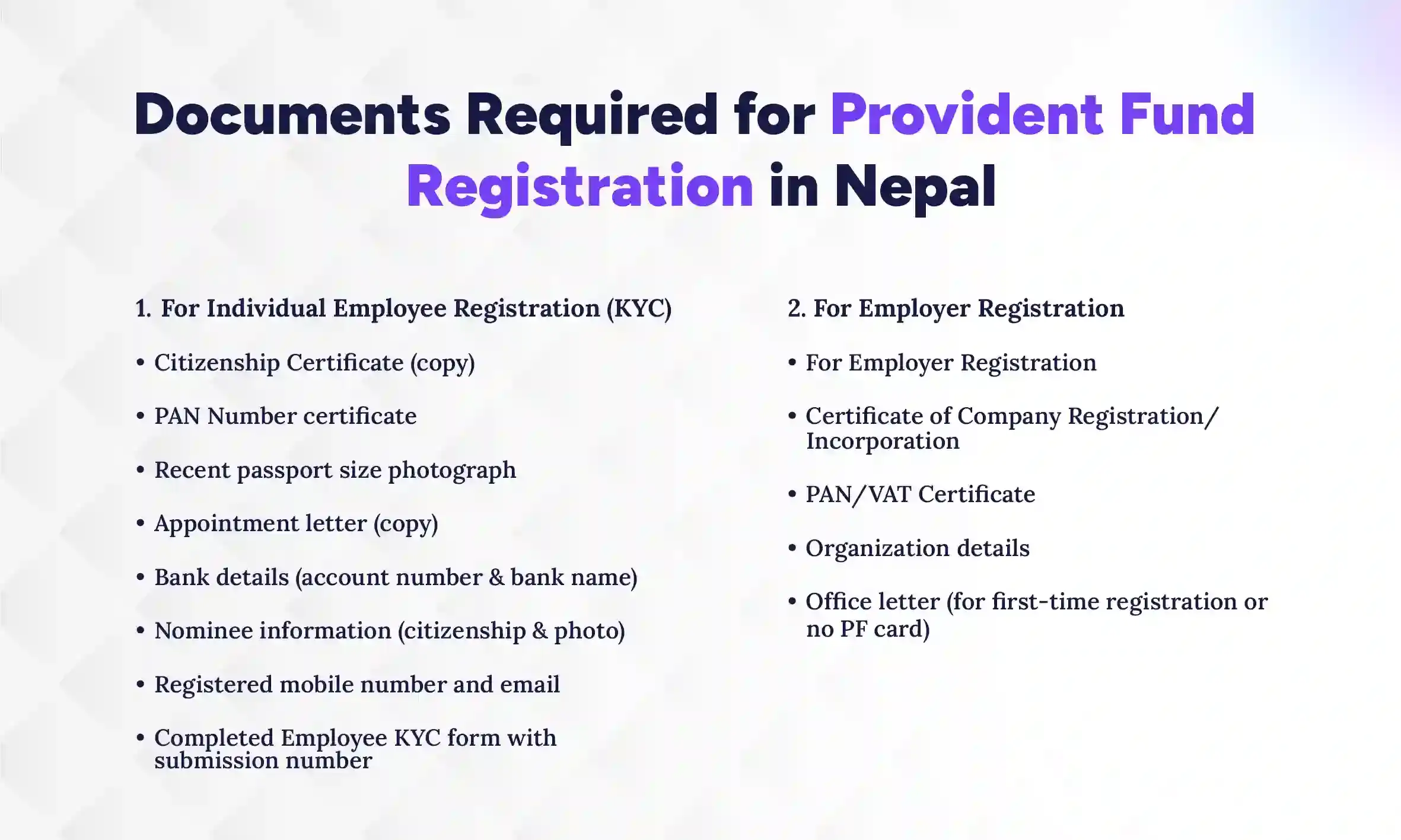

Documents Required for Provident Fund Registration in Nepal

To register for the Provident Fund (PF) in Nepal, both employees and employers must submit certain documents. These ensure proper KYC verification and smooth account setup.

1. For Individual Employee Registration (KYC)

Employees need to submit key documents to verify identity, employment, and bank details, enabling them to open and manage their PF accounts seamlessly.

- Citizenship Certificate: A copy of the employee’s citizenship to confirm legal identity.

- PAN Number: Permanent Account Number certificate for tax and financial records.

- Passport Size Photograph: A recent photo for identification purposes.

- Appointment Letter: Proof of employment through the job acceptance letter.

- Bank Details: Valid bank account number and bank name for PF contributions.

- Nominee Information: Citizenship and photo of the nominee to ensure correct beneficiary allocation.

- Contact Information: Registered mobile number and email for communication.

- Employee KYC Form: Completed online KYC form along with the printed submission number for official record.

2. For Employer Registration

Employers must provide documents that verify the organization’s legitimacy and its authority to manage employee PF accounts. This ensures compliance with PF regulations.

- Certificate of Company Registration/Incorporation: Proof that the company is legally recognized.

- PAN/VAT Certificate: For tax registration and compliance.

- Organization Details: Name, address, and type of business to confirm legitimacy.

- Office Letter: Required if this is the first PF registration or if no PF card exists.

How to Apply for a Provident Fund Online in Nepal?

In Nepal, Provident Fund (PF) registration is typically initiated by the employer. Organizations registered with Employees Provident Fund Nepal enroll their employees and handle the submission process. Employees usually don’t apply independently; instead, they provide required details to their HR or employer, who completes the registration on their behalf.

Step-by-Step PF Registration Process

Here’s how the online PF registration process generally works:

- The employer logs into the EPF Nepal portal

- Employee details are entered into the system

- Required documents are uploaded

- A PF number is generated for the employee

- Monthly contributions begin from salary deductions

Once registered, employees can use their PF number to track contributions, check balances, and access other PF services.

How to Check Employees Provident Fund Balance in Nepal?

Keeping track of your Provident Fund balance is easier than ever. Whether you prefer checking your savings from your smartphone or speaking to someone in person, the Employee Provident Fund (EPF) provides both simple online and offline options to stay updated on your account.

1. Online Method to Check PF Balance in Nepal

The fastest and most convenient way to check your balance is through the official EPF website or their dedicated mobile app. Once your employer has registered your KYC (Know Your Customer) details, you can log in anytime from anywhere.

Here are the exact steps to access your account online:

- Go to the official Employee Provident Fund Nepal website (epfnepal.com.np) or open their official mobile app on your smartphone.

- Navigate to the "Web Login" or "Online Services" section and select the portal designed for contributors.

- Log in by entering your unique PF account number, your username, and your secure password.

- Check your personal dashboard to instantly view your current balance, track monthly deposits, or generate an account statement.

2. Offline Method to Check PF Balance

If you do not have online access, forgot your login details, or simply prefer handling financial matters in person, you can still easily get your account details the traditional way.

Here is how you can request your balance offline:

- Visit your nearest EPF branch office during their regular working hours.

- Bring your official PF identity card and your original citizenship certificate for identity verification.

- Approach the customer service desk to request and receive a printed account statement showing your balance history.

- Alternatively, ask your company's HR department, as many employers receive and distribute annual physical statements from the EPF directly to their staff.

Provident Fund Withdrawal & Tax Rules in Nepal

Managing your Provident Fund (PF) wisely requires knowing when you can access it, how taxes apply, and what eligibility rules you must follow. This guide helps you make informed decisions about your PF in Nepal.

1. What Are the PF Withdrawal Rules in Nepal?

PF withdrawals are allowed during retirement, job change, or special cases, ensuring your savings are protected while giving access when truly needed:

- Retirement: Once you reach retirement age, you can withdraw your full PF amount. This allows you to enjoy the savings you’ve built over your working years.

- Job Change: If you change jobs, you can either transfer your PF to your new employer or withdraw it. This ensures your savings stay secure and accessible, even when your career path changes.

- Special Cases: Emergencies such as serious medical expenses, financial hardships, or company closure may allow early withdrawal. This safety net ensures PF can support you in critical situations.

2. How Can Employees Withdraw PF in Nepal?

Employees can withdraw PF by submitting the application form and required documents to complete the official process:

Step 1: Application Submission

Complete the official PF withdrawal form online or at your PF office.

Step 2: Provide Documents

Submit documents like citizenship, PAN, bank details, and employment proof to verify your identity and eligibility.

Step 3: Processing and Disbursement

Once approved, the PF amount is transferred to your bank account. Following the correct process ensures fast, hassle-free access to your funds.

3. What Taxes Apply on Provident Fund in Nepal?

PF withdrawals are taxable in early or partial withdrawals, and tax-free when withdrawn after retirement or transferred to another employer:

- Taxable Withdrawals: If you withdraw PF early, before retirement, or in certain partial withdrawals, taxes may apply. Knowing this helps you plan financially to minimize liabilities.

- Tax-Free Withdrawals: PF withdrawn after retirement, or transferred to another employer, is usually tax-free. This ensures that your long-term savings retain their full value.

How to Get a Provident Fund Loan in Nepal?

One of the biggest advantages of a Provident Fund is that your money is not entirely locked away until retirement. The Employee Provident Fund (EPF) acts as a financial safety net, allowing you to borrow against your own savings when you face major expenses or emergencies.

1. Who is Eligible for PF Loan and How Much Can You Borrow?

Yes, you can easily take a loan against your accumulated Provident Fund balance. The EPF in Nepal offers different borrowing facilities to active contributors, provided they meet a few basic conditions.

Here is what you need to know about eligibility and the types of loans available:

- You must have completed a certain period of continuous contributions, usually one to two years, to be eligible to apply.

- You are generally allowed to borrow up to 90% of your total accumulated PF balance (which includes both your deposits and earned interest).

- The EPF offers a standard "Special Borrowing" facility for immediate personal or emergency financial needs.

- You can also apply for purpose-specific loans, such as housing loans, educational loans, and medical loans, depending on your situation.

2. EPF Loan Interest Rates and Repayment Rules

Borrowing from your PF is often much cheaper and easier than taking a traditional bank loan. Since you are essentially borrowing against your own money, the approval process is fast, but you are still required to pay interest to ensure your retirement fund continues to grow.

Here is how the interest and repayment terms generally work:

- The interest rate charged on a PF loan is typically just 1% to 1.5% higher than the interest rate the EPF pays on your savings.

- You are required to pay the interest on your borrowed amount on a regular basis to avoid compounding penalties.

- You can repay the principal amount in flexible installments, or arrange for your employer to deduct the loan payment directly from your monthly salary.

- If any loan balance remains unpaid when you retire or leave your job, the EPF will simply deduct the outstanding amount from your final payout.

HR Challenges for Provident Fund & Payroll Management

HR teams struggle with Provident Fund and payroll management because they must constantly calculate exact contributions, follow strict tax laws, and keep employee data completely safe. Even a tiny mistake in these areas can lead to heavy government fines or angry employees who rely on their paychecks. Let us look at the biggest hurdles HR departments face and why handling this money requires so much careful attention.

1. Getting PF Contributions Right

First, HR teams must calculate the exact 10% PF match for both the worker and employer every month. When someone gets a promotion, their basic salary changes, meaning their PF amount must adjust immediately. Furthermore, any calculation mistake directly lowers a worker's retirement savings. Therefore, managers must double-check these numbers to avoid frustrating their staff.

2. Following Government Rules

Next, staying out of legal trouble is a massive daily challenge for HR. They must track new labor laws, changing tax rates, and strict PF rules to stay fully compliant. If they fail to file reports on time, the business faces heavy financial penalties. Because of this, teams spend hours organizing records to pass government audits smoothly.

3. Handling Payroll for Everyone

Additionally, paying different types of workers makes the monthly payroll process very complicated. A company might have full-time staff, part-time helpers, and contractors, each requiring a different payment structure. On top of that, HR must perfectly add overtime and bonuses while subtracting unpaid leave. As a result, calculating everyone's final paycheck takes careful math and focus.

4. Connecting Payroll with PF and Benefits

Another big hurdle is properly linking a worker's payroll account to their PF and health insurance. If someone types the wrong number manually, an employee might miss their retirement deposit. To prevent these costly mistakes, companies must sync all their benefit systems together. Ultimately, ensuring allowances match the payroll record is crucial for employee trust.

5. Keeping Employee Data Safe

Meanwhile, protecting sensitive employee information is more important than ever before. HR holds private bank numbers, salary details, and personal records that hackers want to steal. Consequently, companies must build strong digital walls to stop unauthorized access and prevent data leaks. By strictly following privacy rules, businesses keep their workers' money and identities completely secure.

6. Answering Employee Questions

Finally, dealing with a constant flood of employee questions takes up much of HR's time. Workers frequently ask about their PF balances, confusing tax deductions, and withdrawal rules. To provide clear answers without falling behind on work, HR needs a better system. By setting up automated self-service portals, companies let employees check their own details instantly.

The Smart Solution to PF & Payroll Management: Using an HR Software

Handling all these moving parts by hand is almost impossible for a growing company. That is why smart businesses use HR software to fix these exact problems. An HRMS automatically calculates PF contributions, taxes, and monthly payroll without any costly math errors. Because the software does the heavy lifting, your HR team can finally stop worrying about government fines and focus on supporting your employees.

If you are tired of manual paperwork and confusing spreadsheets, explore how an HRMS reduces paperwork and serves as the perfect tool for your business. It smoothly connects your payroll, benefits, and employee data into one highly secure platform. Plus, it gives your workers a self-service portal to check their own PF balances and payslips instantly, saving everyone time.

Conclusion

Ultimately, a Provident Fund in Nepal is much more than just a retirement account. It is your best tool for building wealth, saving on taxes, and getting free money from your employer. Whether you need a cheap loan today or a safe cushion for tomorrow, your PF has you covered.

Thinking about the future can feel scary, especially when daily bills keep piling up. However, you do not have to worry about growing old without money. By letting your fund work quietly in the background, you are taking a huge step toward financial freedom. Every small chunk saved from your paycheck today is a gift to your future self.

Ready to make your employees monthly payroll fast, accurate, and completely stress-free? Explore Pace HRMS today and see how easy managing your team can be.