Many employees and HR teams in Nepal find managing savings, interest, and retirement plans confusing and time-consuming. Tracking contributions, checking balances, and handling withdrawals can feel like a lot to manage at once. But it doesn’t have to be difficult.

This guide will make it simple. We’ll explain what CIT is, how CIT interest works, and the withdrawal rules in Nepal. You’ll also get practical tips for HR teams managing multiple employees and schemes. We’ll also explore the common HR challenges for managing CIT and payroll, and the solutions in 2026.

What is CIT (Nagarik Lagani Kosh) in Nepal?

CIT, or Citizen Investment Trust, officially called Nagarik Lagani Kosh, is a government-backed fund in Nepal that helps people save money for the future. It is mainly designed for employees who want to build financial security through regular monthly contributions.

Both employees and employers can contribute a part of the salary to CIT. These contributions earn interest over time, which helps the savings grow steadily. On top of that, the scheme provides some tax benefits, making it a smart way to save while reducing taxable income.

CIT works like a long-term retirement savings plan. It ensures that employees have money available after retirement or for specific financial needs. With different schemes under CIT, both individuals and organizations can choose options that suit their goals, making it a safe and flexible investment tool.

What is the Purpose of CIT (Nagarik Lagani Kosh)?

CIT (Citizen Investment Trust), officially known as Nagarik Lagani Kosh, was started in 1968 (2025 BS) under the CIT Act, 1968. It was created to help citizens save money safely. Over time, it has grown to offer several schemes for employees, individuals, and organizations. Its main goal is to help people save for the future, earn interest safely, and support Nepal’s economy.

1. Objectives of CIT for Employees

CIT helps employees save regularly, grow their money safely, and access benefits like interest, bonuses, and loans, making retirement planning and financial security easier.

- Save money regularly for the future.

- Build a secure fund for retirement.

- Earn interest on savings and sometimes get bonuses.

- Reduce taxable income with monthly contributions.

- Get extra benefits like insurance coverage.

- Borrow loans against your CIT savings if needed.

2. CIT Objectives for the Country

CIT encourages national savings, funds government projects, and strengthens Nepal’s economy by reducing reliance on foreign loans.

- Encourage citizens to save money.

- Collect funds for government projects and safe investments.

- Help the economy grow using local savings.

- Reduce the need to borrow money from other countries.

3. Objectives for Foreign Residents / Investors

CIT allows even the foreign residents to safely invest in Nepal while supporting the local economy and earning steady, low-risk returns.

- Allow eligible foreign residents to invest safely in Nepal.

- Support Nepal’s economy through these investments.

- Earn safe returns on their money with low risk.

What Are the Benefits of CIT in Nepal?

CIT provides a reliable way for employees to grow their wealth through tax-free savings while helping employers offer better retirement benefits to their staff. This partnership creates a win-win situation where workers feel financially secure and companies fulfill their legal and social duties. To truly understand why so many people choose this path, let’s look closely at the specific advantages of joining Nagarik Lagani Kosh.

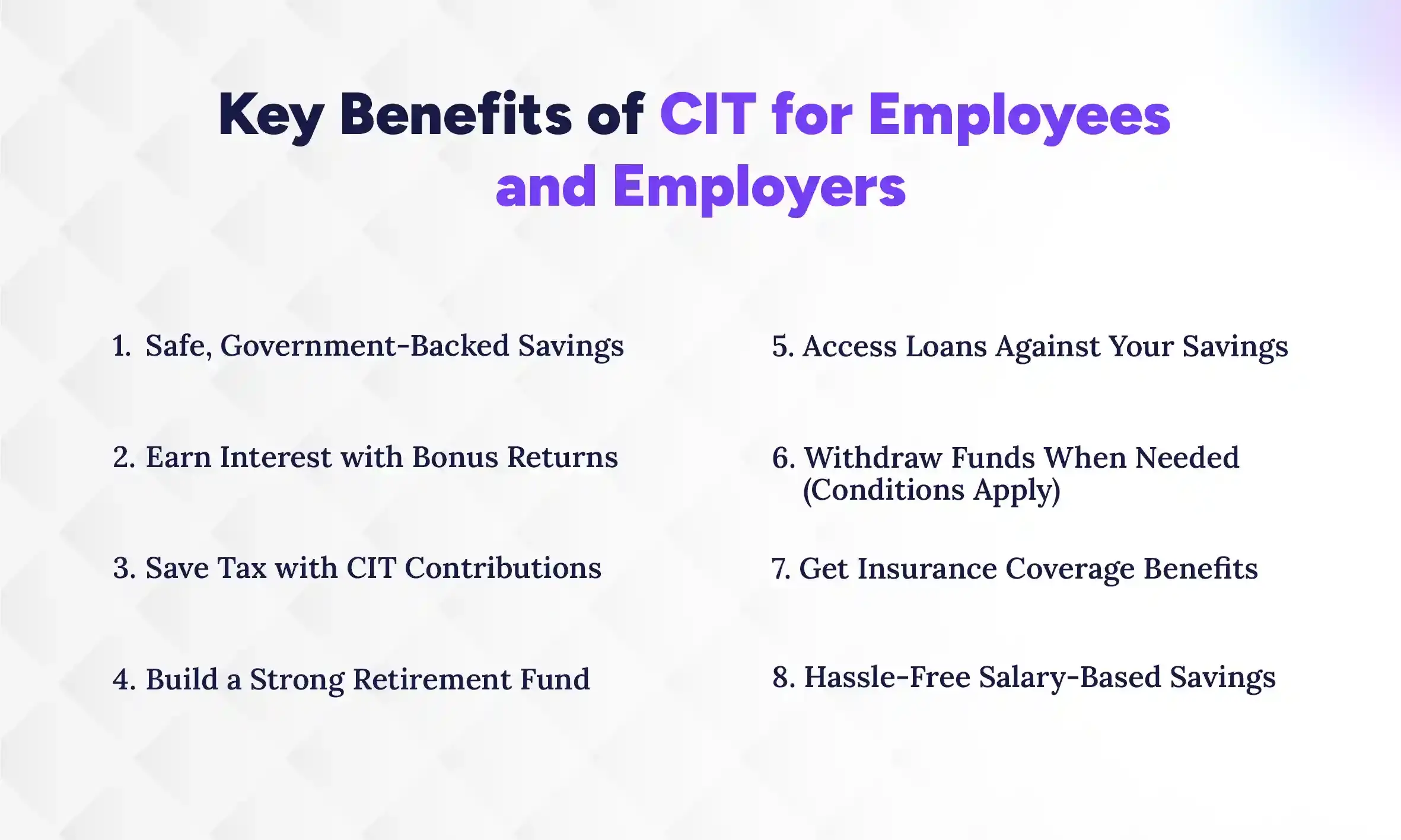

1. Safe, Government-Backed Savings

The Citizen Investment Trust is a highly secure institution because it was created and is monitored by the Nepal government. This means your hard-earned money is protected by law, making it much safer than many private investment options. You can rest easy knowing that your savings are being managed by a trustworthy national organization. Consequently, this high level of safety makes CIT the go-to choice for long-term financial planning for families across the country.

2. Earn Interest with Bonus Returns

When you put money into CIT, your balance grows steadily because it earns a regular interest rate along with extra cash bonuses. CIT takes the collective pool of savings and invests it into profitable sectors like hydropower and banking to generate these returns. Because these profits are shared back with you, your account balance often grows faster than a standard bank savings account. This consistent growth ensures that your small monthly contributions turn into a significant amount of money over time.

3. Save Tax with CIT Contributions

One of the best immediate benefits of joining is that the money you contribute is deducted from your taxable income. By putting money into your CIT account, you legally lower the amount of income tax you have to pay to the government every year. You can save on taxes for contributions up to Rs. 300,000 or one-third of your total annual salary. This smart financial move allows you to keep more of your paycheck today while building wealth for your future.

4. Build a Strong Retirement Fund

The primary goal of CIT is to ensure you have a large sum of money available when you finally decide to stop working. By saving a small portion of your salary every month, you are slowly building a nest egg that will support your lifestyle in your later years. Having this fund ready means you won't have to rely on others for financial help during your retirement. It provides you with the independence and dignity you deserve after a long and successful career.

5. Access Loans Against Your Savings

If you ever face an urgent financial need, CIT allows you to borrow money using your own accumulated savings as collateral. You can quickly access these low-interest loans for important things like home construction, medical bills, or your children's higher education. The process is usually much faster and simpler than applying for a traditional loan at a commercial bank. This feature gives you great peace of mind, knowing that your savings can also help you during emergencies.

6. Withdraw Funds When Needed (Conditions Apply)

While the fund is meant for retirement, CIT provides flexible rules that allow you to withdraw your money under certain conditions. You can generally take out a portion of your total balance after a specific period of service or upon leaving your job. These rules are designed to protect your long-term goals while still giving you access to cash when life changes happen. Having this flexibility makes the scheme a practical choice for workers who want both security and accessibility.

7. Get Insurance Coverage Benefits

Many CIT schemes come with built-in insurance features that provide an extra layer of protection for you and your family. For certain groups like teachers and civil servants, a small part of the contribution goes toward life insurance coverage during their service years. If an unfortunate event occurs, your family will receive a predetermined insurance payout to help them stay financially stable. This combined approach of saving and insuring makes CIT a complete financial package for every working professional.

8. Hassle-Free Salary-Based Savings

Saving money becomes incredibly easy with CIT because the contributions are automatically deducted from your monthly salary by your employer. You don't have to worry about visiting a bank or making manual transfers every month, as the system handles everything for you. This "set it and forget it" method ensures that you never miss a payment and your savings habit stays consistent. It is the most convenient way to build wealth without having to change your daily routine.

CIT Schemes in Nepal: Nagarik Lagani Kosh Programs

CIT in Nepal offers several schemes such as the Employee Savings Fund, Pension Plan, Housing Loan Scheme, and Education/Medical Loan Schemes. These programs are designed to help citizens save regularly, earn interest, and access loans when needed. Let’s take a closer look at each scheme and how it works for employees, employers, and investors:

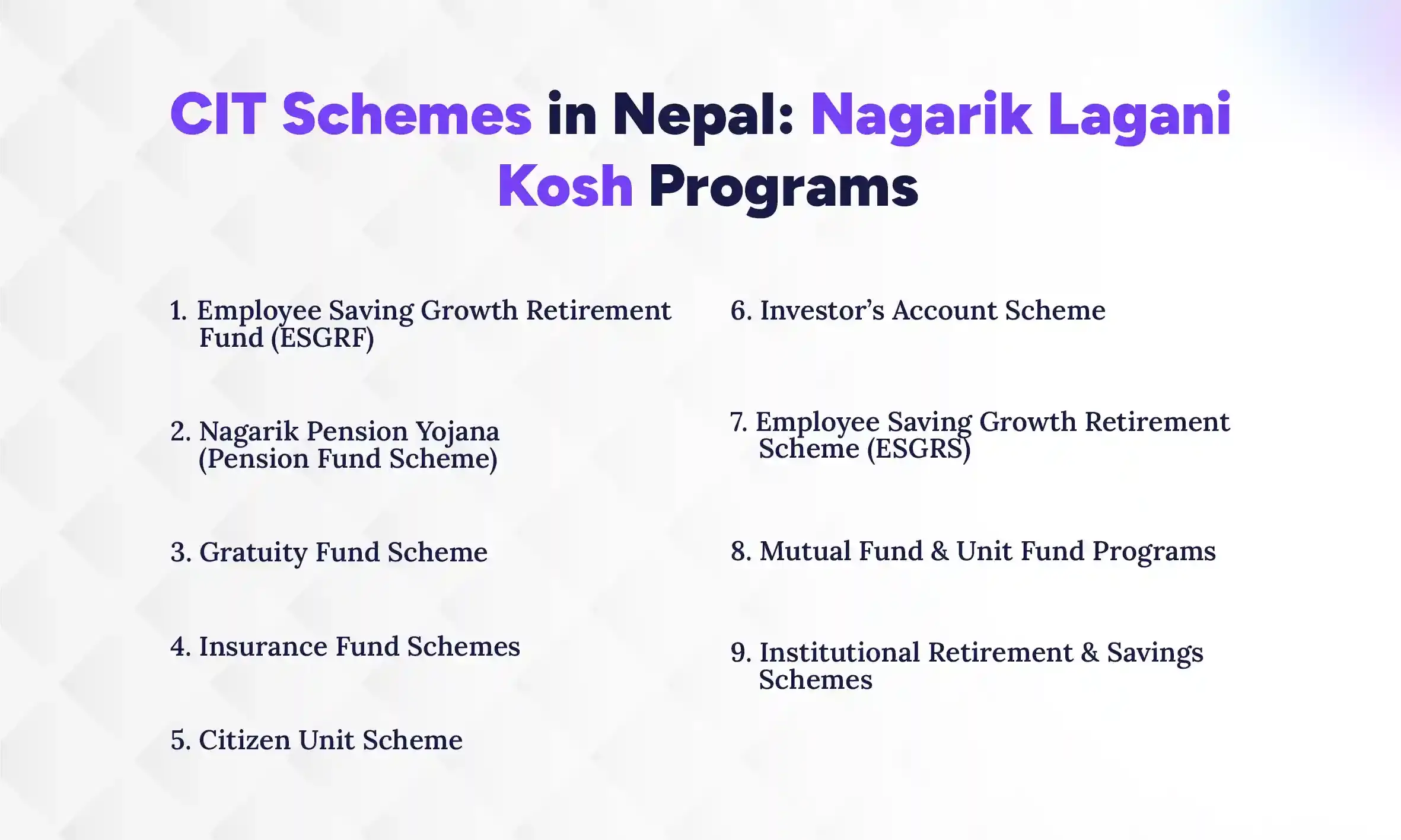

1. Employee Saving Growth Retirement Fund (ESGRF)

The ESGRF is the main long-term savings fund for employees in Nepal. A part of your salary is deposited every month, and your employer adds a matching contribution. Over time, your money earns interest and sometimes a bonus from CIT’s profits. It’s popular because it not only grows your savings for retirement but also gives tax benefits, helping you save more while staying financially smart.

2. Pension Fund Scheme (Nagarik Pension Yojana)

The Nagarik Pension Yojana brings pension benefits to all Nepali citizens, not just government workers. Anyone, including self-employed or informal sector workers, can contribute for at least 15 years. After turning 60, the fund pays a steady monthly pension for life. It’s a simple way to make sure you have financial security and independence in your later years.

3. Gratuity Fund Scheme

Employers in Nepal must pay employees a lump sum when they leave or retire. The Gratuity Fund Scheme lets companies deposit this amount gradually with CIT, instead of paying it all at once. CIT invests the money safely, so the fund grows and is ready when needed. This protects employees and eases the financial load for the employer.

4. Insurance Fund Schemes

CIT offers special insurance-based schemes for public servants like teachers, civil servants, and the armed forces. A small monthly amount is deducted from salaries to provide life insurance and savings. At retirement, employees receive their contributions plus interest, and in case of death, the scheme supports their family. It’s a safe, long-term plan for those who serve the country.

5. Citizen Unit Scheme

The Citizen Unit Scheme is a simple investment option for everyone. You can buy units at Rs. 100 each, and CIT invests the pool into safe sectors of the economy. Investors earn annual dividends, and units can be redeemed anytime. It’s a low-risk, flexible option for people who want better returns than a regular savings account without worrying about the stock market.

6. Investor’s Account Scheme

This scheme is for individuals or organizations with larger funds. CIT manages the account professionally, investing in high-yield options. It’s ideal for trusts, non-profits, and high-net-worth individuals who want a secure, transparent way to grow their money. The focus here is on smart capital growth with professional management.

7. Employee Saving Growth Retirement Scheme (ESGRS)

The ESGRS is a special version of the standard retirement fund, often used for contract-based or institutional employees. It works like ESGRF, building savings through monthly contributions and interest. Companies use it to provide competitive retirement benefits, helping attract and keep talented employees. It’s a reliable way to secure financial rewards at the end of service.

Ready to Simplify CIT Management?

Manage employee contributions, deductions, and compliance with a smarter HRMS solution.

What is the Interest Rate of CIT in Nepal?

CIT (Citizen Investment Trust / Nagarik Lagani Kosh) offers different interest rates depending on the scheme. These rates are generally higher than regular bank savings accounts, making CIT a safe and reliable option for long-term savings.

Interest in CIT is usually calculated on the total account balance and is compounded annually. This means the interest you earn each year is added to your balance, and the next year, interest is calculated on the new total. Over time, this helps your savings grow faster.

Some schemes also offer bonus interest depending on the fund’s performance. This bonus is added to your earnings, increasing the total return on your savings. Together, the regular interest and any bonus make CIT a dependable way to save for retirement or other financial goals.

Current CIT Interest Rates in Nepal

| S.N | Scheme | Interest Rate |

|---|---|---|

| 1 | Employee Saving Growth Retirement Fund | 3.75% |

| 2 | Employee Saving Growth Retirement Fund (90% Loan) | 5.25% |

| 3 | Home Loan | 7.0% |

| 4 | Simple Loan | 7.25% |

| 5 | Citizen Unit Scheme (Individual) | 5.0% |

| 6 | Citizen Unit Scheme (Corporate) | 3.5% |

| 7 | Investor / Endowment Fund | 2.75% |

| 8 | Investor & Endowment Fund Loan (80% Credit) | 4.25% |

| 9 | Insurance Fund (Civil Service) | 2.75% |

| 10 | Insurance Fund (Teachers) | 2.75% |

| 11 | Insurance Fund (Nepal Police) | 2.75% |

| 12 | Insurance Fund (Armed Police Force) | 2.75% |

| 13 | Insurance Fund (Nepali Army) | 2.75% |

| 14 | Insurance Fund (NARC) | 3.75% |

| 15 | Insurance Fund (National Investigation Department) | 2.75% |

| 16 | Citizen Pension Scheme | 4.5% |

| 17 | Simple Loan Endowment | 7.25% |

| 18 | NARC Insurance (80% Loan) | 5.25% |

| 19 | Educational Loan | 7.0% |

| 20 | Vehicle Loan | 7.25% |

This table gives a quick overview of the interest rates across different CIT schemes, helping you decide which scheme is best for your savings or investment goals.

Overall, the CIT interest system is designed to reward long-term savings, provide safe investment options, and give contributors both regular interest and possible bonuses to maximize returns. It helps employees, individuals, and even organizations grow their funds securely over time.

How to Check CIT Balance in Nepal?

Checking your CIT balance in Nepal is easy, and you can do it online, through a mobile app, offline, or even using HR management software. With HR software, employees can access their CIT account details, contributions, and interest directly through the company’s payroll or HR portal, making it fast and convenient. Here’s a detailed guide for each method:

1. Online CIT Balance Check Process

You can check your CIT balance anytime using the official CIT website. Follow these steps:

- Visit the official CIT portal: www.nlk.org.np

- Click on the “Login” or “Account Access” section.

- Enter your username and password provided by CIT or your employer.

- Once logged in, you will see your current balance, total contributions, and interest earned.

- You can also download a PDF statement for your records.

This method is fast, secure, and available 24/7, so you don’t have to visit the office in person.

2. Checking CIT Balance Through HR Management Software

Many organizations now use HR management or payroll software, such as Pace HRMS, which integrates CIT data for employees. With Pace HRMS, employees can:

- Log in to the HR portal or mobile app.

- Access their CIT account summary instantly.

- Track monthly contributions, interest earned, and account balance.

- Download reports or statements directly for personal records.

This method is fast, reliable, and especially useful for employees who want all salary and benefits information in one place without switching between multiple platforms.

3. CIT Mobile App Guide

CIT offers a mobile app for both Android and iOS devices, making it easier to track your savings on the go. Here’s how:

- Download the CIT mobile app from Google Play Store or Apple App Store.

- Open the app and log in with your account credentials.

- Navigate to the Balance/Account Summary section to view your current balance.

- Check the Contribution History to see your monthly deposits.

- Monitor your interest earned and any bonus payments in the same section.

- Some versions of the app also allow you to download statements for record-keeping.

The app is convenient for employees who want real-time updates without relying on their employer or visiting the office.

4. Offline Methods to Check CIT Balance

If you prefer offline methods, you can also check your CIT balance without using the internet:

- Ask your employer or HR department to provide your latest CIT account statement.

- Visit the nearest CIT office and bring your account details or identification.

- The CIT staff will provide your current balance, contribution history, and interest earned.

- You can request a printed account statement for your records.

Offline methods are useful for those who may not have internet access or prefer in-person assistance.

Can You Take Out Money from CIT: Withdrawal & Loan Rules

CIT (Nagarik Lagani Kosh) allows employees and investors to access their funds under certain conditions. Whether you want to withdraw your full savings or take a partial withdrawal or loan, there are clear rules to follow. Understanding these rules helps ensure you use your CIT funds safely and correctly.

1. CIT Withdrawal Rules in Nepal

Full withdrawal of your CIT balance is generally allowed in the following situations:

- Retirement: Once you reach the retirement age, you can withdraw your entire savings along with the accumulated interest and bonuses.

- Job Termination: If you leave your current job, you are eligible to withdraw the balance contributed by you and your employer.

- Meeting Specific Eligibility Conditions: CIT may have other conditions, such as certain years of contribution, for full withdrawal.

Full withdrawal ensures that contributors can access their retirement savings or accumulated funds when they need it most, making CIT a dependable long-term investment.

2. Partial Withdrawal and Loan Facilities

CIT also allows partial withdrawals or loans without closing the entire account. This is helpful in situations where you need funds temporarily:

- Medical Emergencies: If you or a family member faces unexpected medical expenses, you can withdraw part of your balance to cover costs.

- Education Expenses: Partial withdrawal or loans can help pay tuition or other education-related costs for yourself or family members.

- Housing Needs: You can take a loan or withdraw funds for home construction, renovation, or purchasing a house.

Partial withdrawals and loans are designed to give contributors flexibility while keeping the account active and continuing to earn interest.

3. Required Documents for CIT Withdrawal

To make a withdrawal or request a loan, you need to submit some documents to CIT or through your employer:

- Copy of Citizenship: Proof of identity is required for all transactions.

- Employment Verification: A letter or document from your employer confirming your employment or termination status.

- CIT Account Details: Include your account number and relevant CIT scheme information to process the withdrawal accurately.

Submitting the correct documents ensures a smooth and timely withdrawal process. Some cases may require additional papers depending on the type of withdrawal or loan requested.

Overall, CIT provides a flexible yet secure system for accessing your funds. You can withdraw fully at retirement or job termination, or take partial withdrawals and loans for urgent needs, all while continuing to grow your savings safely.

What Are the Common HR Challenges in Managing CIT?

Managing CIT contributions and accounts can be challenging for HR teams, especially when handling multiple employees, schemes, and compliance rules. HR professionals must ensure accuracy, timeliness, and transparency to avoid mistakes and keep employees satisfied. Below are the main challenges they face and why they matter.

1. Mistakes in Calculating Contributions

When HR calculates CIT contributions manually, mistakes can easily happen. Miscalculating percentages of salary, interest, or employer contributions can lead to underpayment or overpayment. These errors may cause confusion for employees and extra work to correct records. Using automated payroll tools or double-checking each calculation can reduce errors and ensure accuracy.

2. Late Deposits of Contributions

Delays in depositing CIT contributions can create trust issues with employees and may lead to penalties from the government. HR teams often face challenges coordinating with payroll schedules, banks, or CIT offices. Even small delays can affect interest calculation and employee satisfaction. Implementing strict timelines and automated reminders can help ensure deposits are made on time.

3. Keeping Up With Compliance Rules

CIT contributions must follow government rules, including deadlines, eligible amounts, and documentation requirements. Tracking compliance manually is time-consuming and prone to mistakes, especially for companies with many employees. Missing deadlines or incorrect filings can result in fines and audits. HR teams need a clear system or software to monitor compliance consistently and reduce risk.

4. Managing Different CIT Schemes

Many organizations have employees enrolled in different CIT schemes simultaneously, each with its own rules and interest rates. Keeping track of contributions, withdrawals, and loan eligibility for each scheme can be complex. Mistakes in applying scheme rules can frustrate employees and create reconciliation issues. Using integrated HR software helps manage multiple schemes efficiently and accurately.

5. Answering Employee Questions

Employees often have questions about their CIT balance, interest calculation, or withdrawal eligibility. Answering these queries manually takes time and can slow down HR operations. Inaccurate or delayed responses can reduce trust and satisfaction. Providing self-service portals or using HRMS platforms can streamline query management and improve transparency.

6. Working Closely With Finance Teams

CIT management requires close coordination between HR, finance, and payroll teams. Miscommunication can lead to incorrect deductions, delayed contributions, or missing documentation. Ensuring that all teams have updated records and follow standard procedures is essential. Regular communication, shared dashboards, and automated reports can help maintain smooth coordination.

How to Simplify CIT & Payroll Management in Nepal?

HR teams can simplify CIT contributions and payroll in Nepal using tools like Pace HRMS, Excel templates, or well-defined SOPs. The easiest and most efficient way to manage payroll in 2026 is smart and modern HR software.

With an HRMS, HR teams no longer need to manually calculate contributions, track interest, or follow up on deadlines. Everything is automated, from monthly deposits to interest accrual and bonus tracking. Employees can also check their balances, contributions, and interest directly through the HR portal or mobile app, making the whole process transparent, smooth, and reliable for everyone.

Which is the Best HR Management Software for CIT & Payroll in Nepal?

Pace HRMS stands out as the most reliable HR management software for managing CIT and payroll in Nepal. The tool helps HR teams automate calculations, manage multiple schemes, and keep compliance on track without extra effort.

It also provides employees with self-service access to their account balances, contributions, and interest, reducing repetitive HR queries. The software combines payroll, CIT management, and reporting in one platform, making it easier for HR and finance teams to work together efficiently.

Moreover, since the tool is designed with inputs from some of the top HR professionals in Nepal, Pace HRMS rightly meets the Nepalese HR requirements. The software has set a benchmark for Nepalese HR tools, clean UI, easy navigation, simplified features, and excellent customer support.

Features & Benefits of Pace HRMS

Pace HRMS offers a range of tools that simplify CIT and payroll management:

- Automated Calculations: Accurately computes employee and employer contributions, interest, and bonuses.

- Timely Deposits: Schedules contributions and sends reminders to ensure no delays.

- Compliance Tracking: Monitors deadlines, contribution limits, and required documents automatically.

- Multi-Scheme Management: Tracks different CIT schemes, loans, and withdrawals for all employees.

- Employee Self-Service: Employees can view balances, contributions, and interest reports anytime via portal or mobile app.

- Finance Coordination: Shared dashboards and automated reports align HR and finance teams.

- Document Management: Stores citizenship copies, employment verification, and account details digitally for quick access.

With these features, Pace HRMS makes CIT and payroll management simple, accurate, and stress-free, benefiting both HR teams and employees alike.

Conclusion

CIT in Nepal is more than just a savings scheme, it is a reliable way to grow your money, earn interest, and secure your future. This guide has shown how employees and employers can manage contributions, check balances, and use loans while staying compliant and organized.

For individuals, CIT encourages disciplined saving and gives access to loans when needed, making financial planning easier and more secure. For HR teams, integrating CIT into payroll ensures accuracy and reduces stress, keeping both employees and management happy.

Using Pace HRMS makes all of this simple for employees as well as HR teams. With automation, compliance tracking, and easy employee access, it helps HR manage CIT and payroll efficiently, so your team can focus on what really matters.

Ready to adopt an HR software? Explore this guide to the best HR software for small businesses in Nepal.